➤ SIGNAL

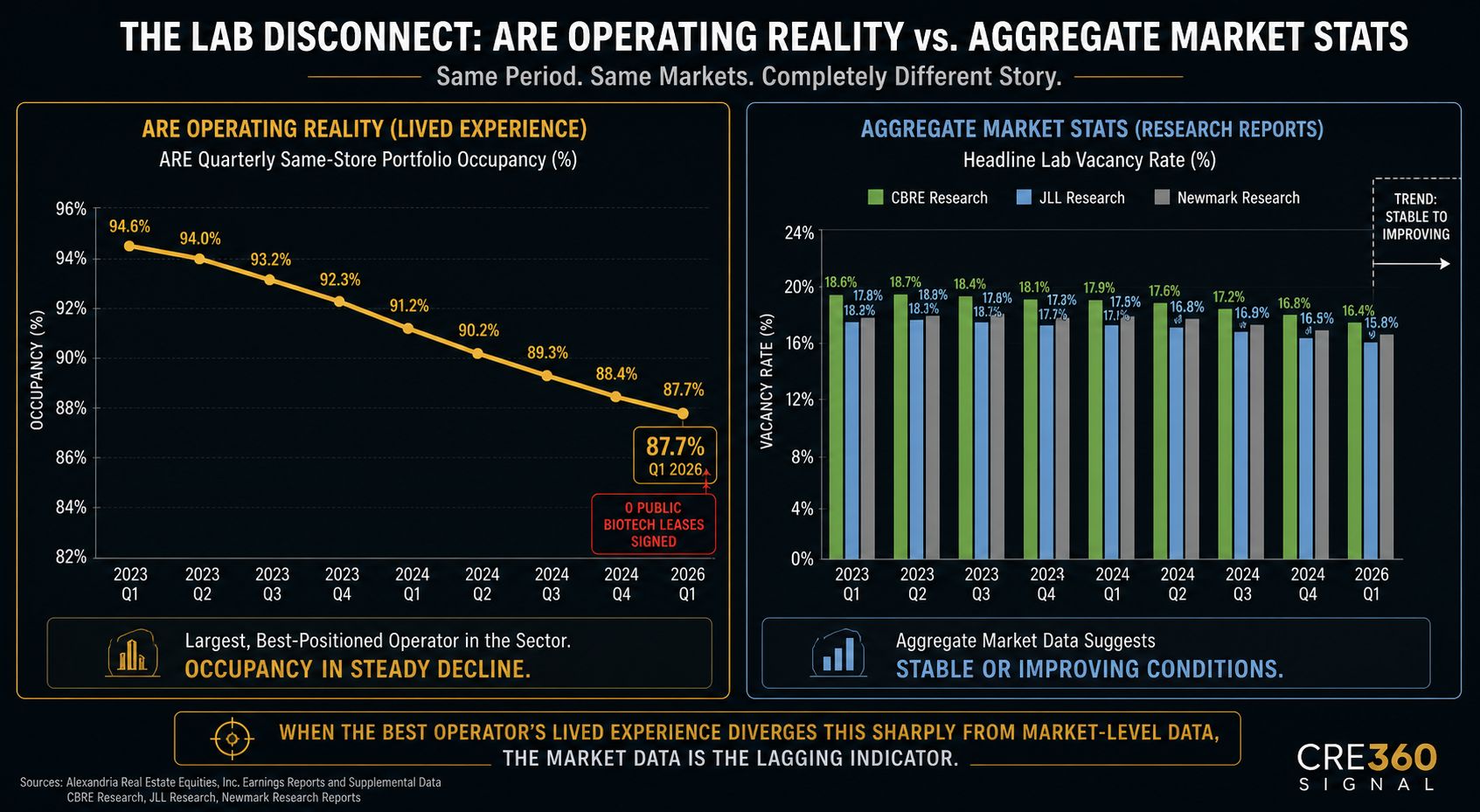

The largest pure-play lab REIT in the country, operating in the strongest lab submarkets in the world, signed zero new leases with public biotech tenants in a 90-day window. That's not a softening market. That's a frozen one.

The aggregate CBRE/JLL/C&W lab vacancy stats have been telling a "we're near the bottom" story for two quarters. Alexandria's Q1 print contradicts that directly. When the operator with the best portfolio, the deepest tenant relationships, and the most disciplined development pipeline cannot move a single public biotech lease across the line, the diagnosis isn't market softness — it's tenant paralysis. Public biotechs aren't slow-walking decisions. They're not making them. NIH/FDA leadership turnover, capital-markets stress, and clinical-trial timing have collectively removed the buyer from the table.

Implications for CRE:

Lab cap rates need a wider repricing than consensus assumes. If ARE's portfolio underperforms by this much, second- and third-tier lab assets (Boston suburbs, Research Triangle, San Diego periphery) face cap rate widening of 100–150 bps from current marks.

The sublease overhang is structural, not cyclical. With known 2026 expirations of 747K SF on top of Q1 vacancies, sublease supply gets worse before it gets better — pressuring direct rents into 2027.

Spec lab development is over for this cycle. Any lab project not pre-leased to an investment-grade tenant should be paused, repositioned to flex/R&D, or value-engineered down. The basis math doesn't work at current absorption.

Conversion plays die. Office-to-lab repositioning was a 2023–2024 thesis. With ARE's stabilized assets at 87.7%, no rational lender funds a Class B office converting to spec lab in 2026.

The capitalized-interest cliff is a forced sell signal. ARE moving $1.5B off the development pipeline means $1.5B less depreciation shield and $1.5B more pressure to lease or dispose. Watch for Megacampus dispositions in 2026 H2.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market. Key Takeaways

- “When the best operator in the asset class prints the worst quarter in its history, the issue isn't operational — it's structural. Lab is not bottoming. It's still finding the floor, and underwriters pricing 2026 lab acquisitions to consensus stats are pricing to the wrong number.”

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.