➤ SIGNAL

The largest AI infrastructure partnership in the world quietly closed a Michigan transaction the same week Northern Virginia lost its largest planned campus. That's not a coincidence — it's a capital reallocation event playing out in public.

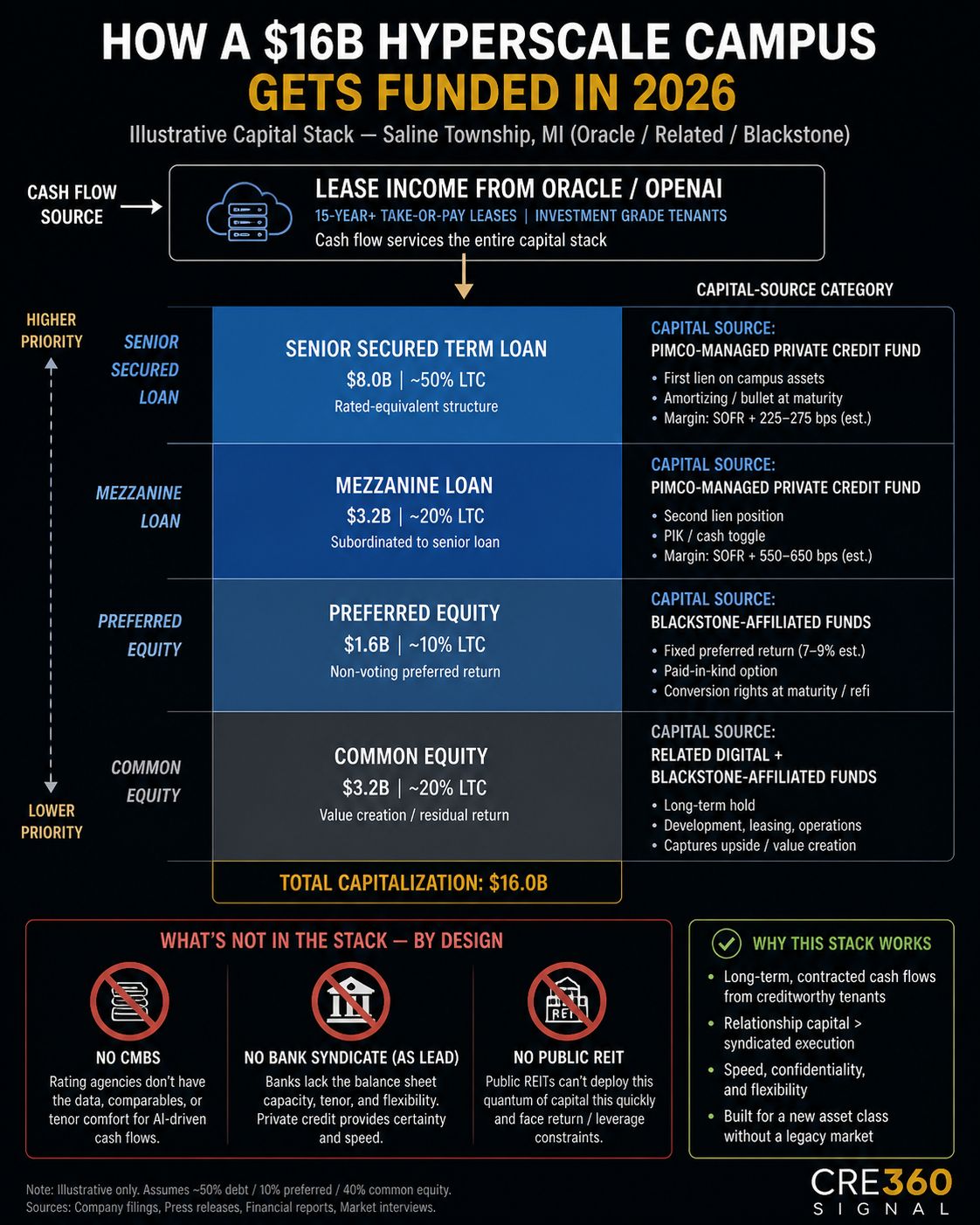

The headlines on this story focus on Oracle, OpenAI, and the size. The underwriting story is the capital stack. Equity from a developer-operator partnership (Related Digital + Blackstone). Debt anchored by PIMCO-managed private credit. No CMBS. No public REIT balance sheet. No bank syndicate as the lead. The dominant capital source for AI hyperscale is now private credit fronted by a small number of mega-managers, and that has implications for every developer trying to compete for hyperscale tenants without that relationship.

Implications for CRE:

Private credit owns hyperscale debt. PIMCO, Apollo, Blackstone Credit, and a handful of others are now the price-setters for $1B+ data center debt. CMBS issuers and bank syndicates are reduced to the second tier — fine for stabilized assets, structurally locked out of pre-lease/construction takeouts at this scale.

Developer relationships matter more than balance sheets. Related Digital didn't win this on capital alone — they won it on entitlement execution, power procurement, and operator partnership. Mid-tier data center developers without those three legs are not competing for Stargate-scale work, regardless of capital access.

Michigan, Indiana, Ohio are now Tier-1 AI compute geographies. Saline Township and Lebanon close within a week of each other; Central Ohio is already deep into the Intel/AWS buildout. The Midwest corridor is no longer "emerging" — it's the de-facto #2 U.S. hyperscale market behind Northern Virginia, and it's where the next $50B of capital deploys.

Power procurement is the developer's moat. A 1 GW campus requires utility partnership, transmission infrastructure, and often on-site generation. The developers who locked up power positions in 2023–2024 are now executing; the ones who didn't are buying secondary land at premium basis with no path to interconnection.

Land basis in emerging Midwest markets reprices upward. Saline, Lebanon, and Columbus-adjacent parcels with utility-served entitlements just had a comp printed at scale. Sellers tighten; buyers either pay or move to tertiary markets.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market. Key Takeaways

- “The AI infrastructure buildout isn't a Texas-and-Virginia story anymore — it's a Midwest story funded by private credit through a narrow group of operator-developers. If you're not in that capital stack or in those geographies with power locked up, you're not in the trade.”

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.