➤ SIGNAL

Recent presale and final rating releases from Fitch Ratings around deals like GGP Trust 2026-2PAK and PRPM 2026-CRE1 are giving a very clear signal:

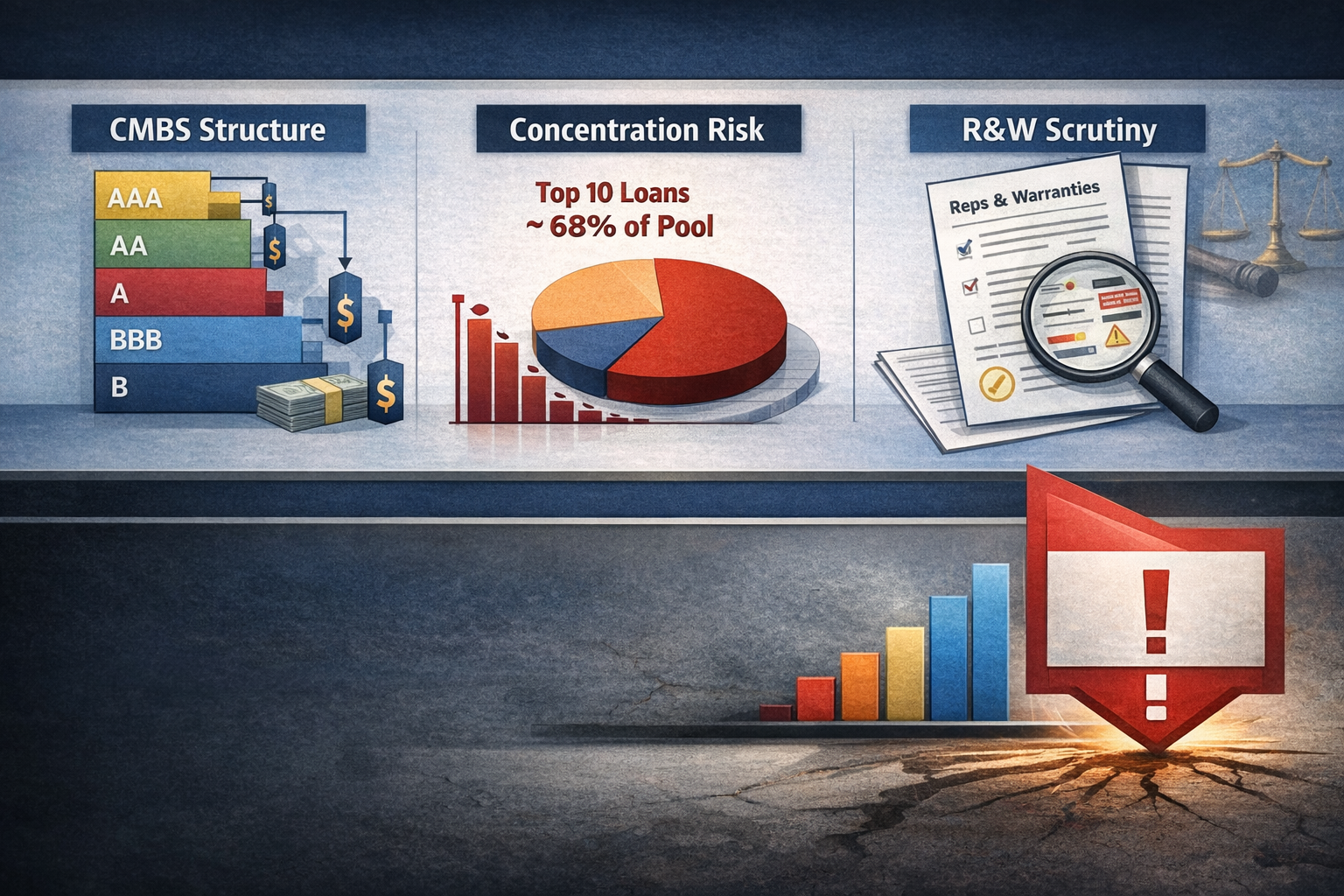

This market is not recovering evenly — it’s concentrating risk.

The PRPM CRE CLO shows top-10 loan concentration approaching ~68–70% of the pool. That’s not just a statistic — it changes how these deals behave under stress. One or two asset failures can materially impair performance, especially in transitional or value-add collateral.

At the same time, the GGP Trust deal includes expanded R&W disclosures. That matters more than people think — it tells you lenders and rating agencies are focused on what breaks legally and structurally when things go wrong, not just underwriting assumptions.

Here’s the key shift:

This is no longer a market of broad credit expansion

It’s a market of structured risk packaging

Deals are getting done — but they’re being engineered, not broadly financed.

From an operator standpoint — not capital markets theory — this creates a very specific environment:

Loan selection matters more than market direction

Asset-level underwriting beats portfolio diversification narratives

Structure (triggers, covenants, waterfalls) becomes as important as DSCR

If you’re evaluating deals or raising capital:

You’re not competing on access to money

You’re competing on how defensible your asset is inside a stressed capital stack

And here’s where most people get it wrong:

They assume more deals = more liquidity = safer market.

That’s not what’s happening.

More deals right now = more selective capital chasing fewer “clean” assets

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market.Key Takeaways

- “Expect continued issuance , but with tighter structures and heavier concentration”

- “Expect more dispersion in outcomes — winners and losers won’t be correlated”

- “Expect capital to reward execution clarity , not just projections”

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.