➤ SIGNAL

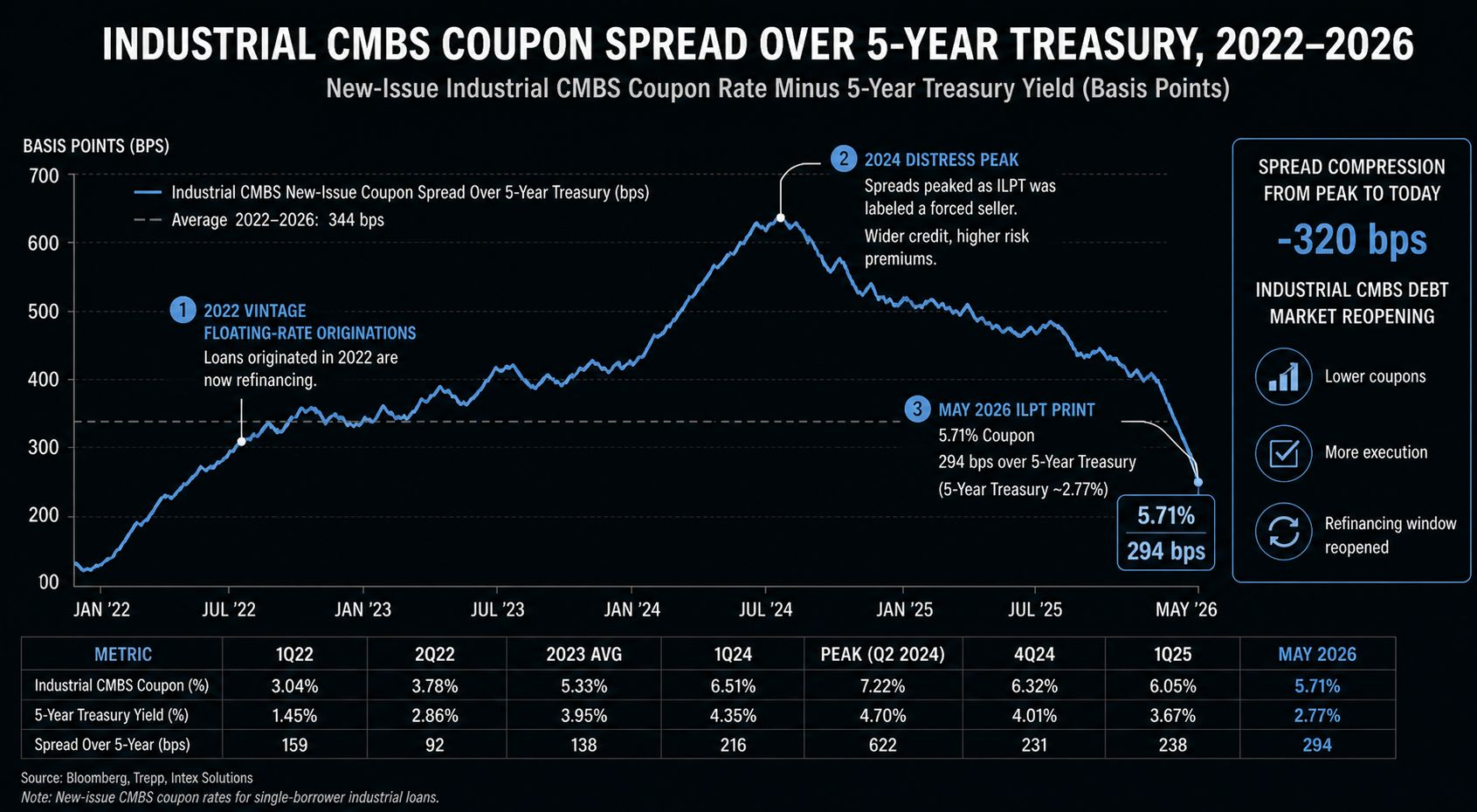

A stressed-balance-sheet logistics REIT just printed a $1.6B fixed-rate CMBS at a 5.71% coupon and 75.3% LTV — and the syndicate filled. That tells you the CMBS bid for high-quality industrial is back, at a price that wasn't available six months ago.

Our angle: The headlines focus on ILPT specifically. The underwriting story is the public comp. There is now a verifiable 2026 benchmark for what investment-grade Class A logistics debt costs: 5.71% fixed at 75% LTV, IO, five-year. Every Mapletree, Dalfen, EQT, and family-office industrial portfolio coming to market gets priced against this number. Sellers can't claim tighter coupons exist; buyers can't claim wider ones do. The comp is locked.

Implications for CRE:

Industrial cap rates have a defensible debt anchor again. Plug 5.71% debt at 75% LTV into a 6.0–6.25% cap rate, and the levered yield math works for institutional buyers. That math hasn't worked cleanly since mid-2023.

The "stressed REIT can't refi" thesis is partially wrong. ILPT was the poster child for forced sellers in 2024–2025 commentary. They just refinanced $1.6B and saved $20M annually. Distress narratives need to distinguish between asset class and operator — ILPT's portfolio is fine; its prior capital structure wasn't.

Floating-to-fixed conversion is now the dominant industrial refi trade. Any portfolio still on a floating-rate facility from the 2021–2022 vintage is paying for the option to refinance — and the option just got cheaper to exercise. Expect a wave of similar conversions across the next two quarters.

Watch the Fitch projection vs. the print. Fitch projects industrial CMBS delinquencies rising from 3.5% to 4.6% in 2026. ILPT just priced through that projection at a tight spread. The high-credit segment of industrial (FedEx, Amazon, Home Depot tenant base) is decoupling from the broader index — which means the index will increasingly mask the bifurcation.

Class A industrial is closer to the bottom than consensus thinks. Prologis Q1 said vacancy is peaking near 7%, large-format space is effectively sold out at 98% leased globally. ILPT's debt print is the financial confirmation of the operational thesis — a CMBS market doesn't price aggressively into a deteriorating asset class.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market. Key Takeaways

- “The industrial cycle inflection isn't theoretical anymore — it's priced. A 5.71% public benchmark on a stressed-REIT portfolio means Class A logistics debt is open for business, and the next round of industrial M&A and recap activity now has a number to underwrite against.”

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.